What If The Sector Looks Strong but Ethically Questionable?

3 min read

Before anything else, here are three trading rules I always try to practice.

It’s not about being right, it’s about making money.

Taking a loss is part of the process.

Never sell the strongest markets until it fails.

Now that being said, I acknowledge the volatility the market is currently facing and will continue to face this month. For a few months now I’ve been considering phasing out exposure to companies whose products directly erode human health. I’m talking about companies like:

Coca-Cola

PepsiCo

McDonald's

KFC

Burger King

The Sector is technically Consumer Staples. But specifically, I’m referring to the food and beverage industry. Why? It is after all considered a defensive and/or safe haven Buy.

Investors typically rotate into these stocks to safeguard portfolios during economic uncertainty or high market volatility as they exhibit:

Lower beta ✅

Stable demand ✅

Consistent dividends ✅

Do I really need to help you arrive at a cohesive investment argument that explains why divesting from these securities (or ETFs that hold them) would be great for your portfolio in the long-term but also good for the people?

Let me give it a shot.

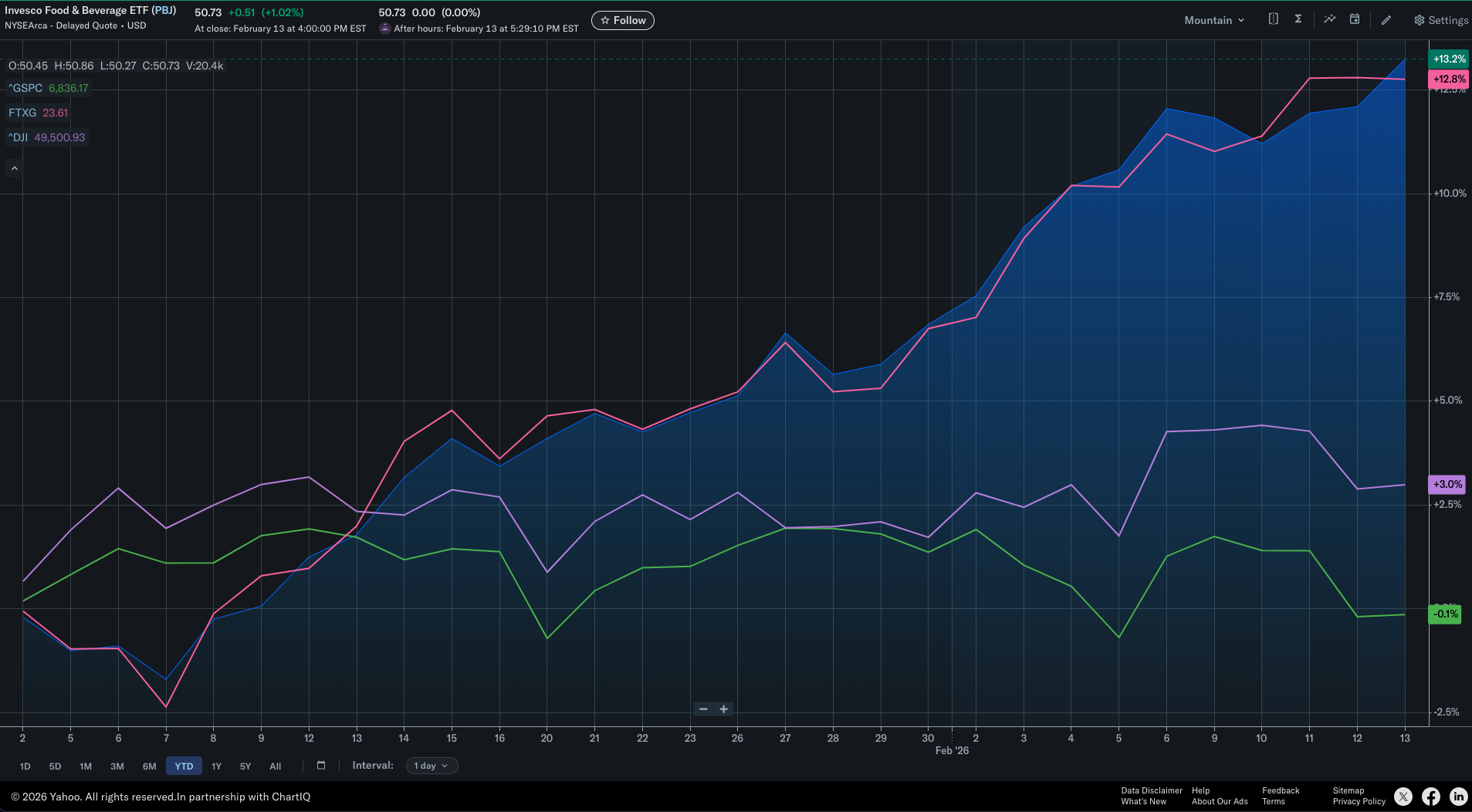

Year-to-Date $PBJ and $FTXG are up 12–13%, compared to the S&P 500 that is flat and the DOW that’s up a modest +3.0%.

On the surface, the sector is far from weak. In fact $FTXG is actually overperforming the broader Consumer Defensive category, which is up over 7% just in the last month. For me the sector isn’t weak in isolation, but it appears increasingly crowded and fully valued.

My concern isn’t purely technical but more of a fundamental argument. These companies continue to lose market share to clean label and private-label competitors. Recent acquisitions, such as PepsiCo’s purchase of Siete Foods suggest incumbents are buying growth rather than generating it organically. When long-term allocators reassess legacy food brands, it raises the question of whether the durability of those cash flows is changing.

For a long while now, these large corporations (Big Food) have had such exponential growth that the quality of their product has suffered when compared to their business operations. I could hammer my point by attempting to anchor my narrative with a recent headline. For example, Did you know that Berkshire Hathaway is selling the remainder of their investment of the kraft Heinz company? That’s ~325 million shares. But of course, that case is unique and I’m certain there are way more variables involved.

Is my consideration to divest financially rational or emotionally reactive?

As of last week, the Consumer Staples sector is trading at its highest valuation since the 2000 bubble. Investors have crowded into these names out of fear, seeking shelter from the "AI fatigue" hitting large-cap tech. But when the sector becomes this expensive, the safety evaporates. I’m not just selling because the food is a net-negative for humanity; I’m selling because the market is asking me to pay a premium for a product whose quality is facing increasing consumer scrutiny.

In a world demanding transparency, "Big Food" is the most exposed. The shift is already fiscal and legislative:

The GLP-1 Factor: 12% of Americans are now on medications that materially alter consumption patterns and their relationship with processed sugar and salt.

The SNAP Lockdown: As of last month, 18 states have begun blocking taxpayer funds from being spent on sugar-sweetened beverages.

The defensive trade of the last decade may be entering early-stage decay.

I won’t outright sell strength, but I beginning to reduce exposure before full confirmation hits the tape. Risk management sometimes requires anticipation, not reaction.

Are you looking to rebalance out of this sector? Let’s talk